The Houston real estate market in 2016 achieved a record volume despite the oil patch downturn and 2017 is shaping up to be another great year. Looking at full year data from 2015 versus 2016, single family home sales were up 3% wi...

Fellow Agents - this is some information from one of my preferred lenders. Diane always sends out great information and is a great educator and resource. I would highly recommend her.

I get lots...

According to the Houston Association of Realtor March market report, sale volume for Single Family Homes was still positive (particularly in the $150-$500K range) despite the strain on jobs in the oil field. &n...

First of all, let me say that this is an article for agents by an agent. After going through a buyer's market and now a seller's market, I prefer the buyer's market. Yes it's great getting a house sold quickly...

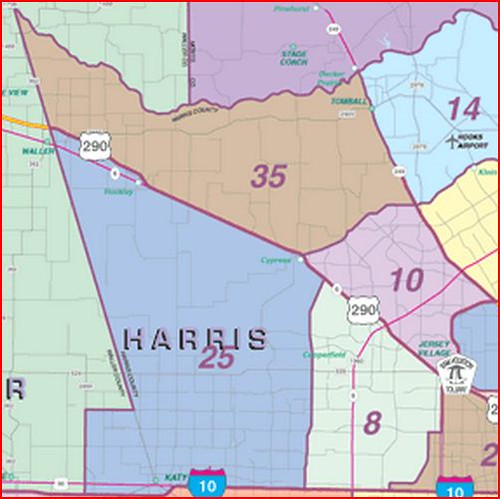

Despite falling oil prices and layoffs, Houston and the North to West quadrant of Houston are still experiencing strong sales. Prices for single family homes are significantly higher over last year in the Multiple Listing Service a...

Hello my name is Carmen Donaldson. I have been a local, full time realtor with Keller Williams since 2007.

I understand that selling your home can be one of the most personal and important transactions in a pe...

One of the least expensive and most impactful things an owner can do when getting their home ready to sell is painting. Painting gives the home a fresh feeling and a clean smell; both very important to prospective buyers. I h...

At the end of last year, I helped a first time homebuyer who was able to close with exactly 3.5% (FHA Loan) on a $160,000 home. That made me curious to see how much cash my other buyers (in the past 2 years) had to bring to the clo...