The market is still strong, prices are going down, just a tad. Click link below the to read the full press release.

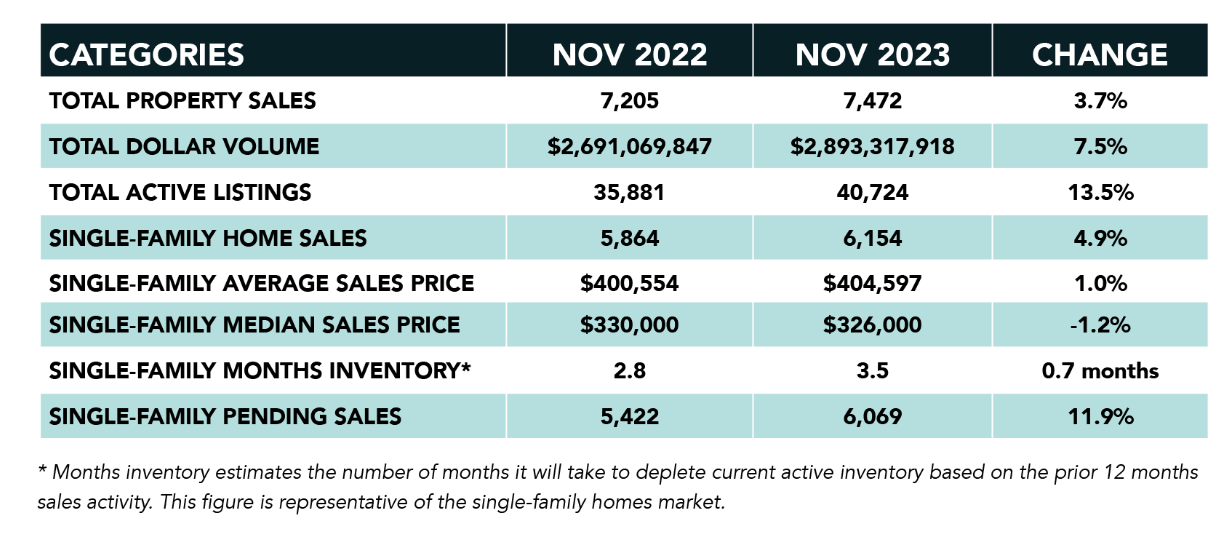

Months of inventory expanded from a 2.8-months supply last November to 3.5 months, matchi...

For full report click below.

https://www.har.com/blogs/detail?id=118539&blogpreview=1

As...

If you buy now and mortgage rates don't change: You made a good move since home prices are projected to grow with time, so at least you beat rising home prices.

If you buy now and mortgage rates fall (as projected):...

Securing your dream home comes with the responsibility of understanding the intricacies of the homeowners insurance cost. When protecting your home, homeowners insurance is your shield against the unexpected. But have you ever wondered w...

Every homeowner must understand the critical role of interest rates in mortgage refinancing.Mortgage interest rates can impact the practicality, benefits, and potential savings of recapitalizing your home loan.Homeowners ne...

Watch video click on link below.

https://youtu.be/rKFg-MmXRrc...

You’ve heard of buyer’s remorse; but without your market expertise and sales skills to back them up, sellers who choose to sell their home on their own just may experience “seller’s regret” when they see how much less they get...

If you are a dog lover and you love to walk your dog -

The old Clear Lake Golf Course is a pretty cool spot -

Additionally learn more about future improvements Exploration Green...

Uno enjoying a walk along the "Old Clear Lake Golf Course"

Did I mention?

I am a pet friendly REALTOR®

I understand the love you have for your pet, and I'll do my best to make sure you're BO...